SARFAESI Act

The Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (SARFAESI) empowers Banks / Financial Institutions to recover their non-performing assets without the intervention of the Court. The Act provides three alternative methods for recovery of non-performing assets, namely: –

- Securitisation

- Asset Reconstruction

- Enforcement of Security without the intervention of the Court

The provisions of this Act are applicable only for NPA loans with outstanding above Rs. 1.00 lac. NPA loan accounts where the amount is less than 20% of the principal and interest are not eligible to be dealt with under this Act.

Non-performing assets should be backed by securities charged to the Bank by way of hypothecation or mortgage or assignment. Security Interest by way of Lien, pledge, hire purchase and lease not liable for attachment under sec.60 of CPC, are not covered under this Act

The Act empowers the Bank:

- To issue demand notice to the defaulting borrower and guarantor, calling upon them to discharge their dues in full within 60 days from the date of the notice.

- To give notice to any person who has acquired any of the secured assets from the borrower to surrender the same to the Bank.

- To ask any debtor of the borrower to pay any sum due or becoming due to the borrower.

- Any Security Interest created over Agricultural Land cannot be proceeded with

If on receipt of demand notice, the borrower makes any representation or raises any objection, Authorised Officer shall consider such representation or objection carefully and if he comes to the conclusion that such representation or objection is not acceptable or tenable, he shall communicate the reasons for non acceptance WITHIN ONE WEEK of receipt of such representation or objection.

A borrower/guarantor aggrieved by the action of the Bank can file an appeal with DRT and then with DRAT, but not with any civil court. The borrower/guarantor has to deposit 50% of the dues before an appeal with DRAT.

If the borrower fails to comply with the notice, the Bank may take recourse to one or more of the following measures

- Take possession of the security

- Sale or lease or assign the right over the security

- Manage the same or appoint any person to manage the same

Background

With an aim to provide a structured platform to the Banking sector for managing its mounting NPA stocks and keep pace with international financial institutions, the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest (SARFAESI) Act was put in place to allow banks and FIs to take possession of securities and sell them. As stated in the Act, it has “enabled banks and FIs to realise long-term assets, manage problems of liquidity, asset-liability mismatches and improve recovery by taking possession of securities, sell them and reduce non performing assets (NPAs) by adopting measures for recovery or reconstruction.” Prior to the Act, the legal framework relating to commercial transactions lagged behind the rapidly changing commercial practices and financial sector reforms, which led to slow recovery of defaulting loans and mounting levels of NPAs of banks and financial institutions.

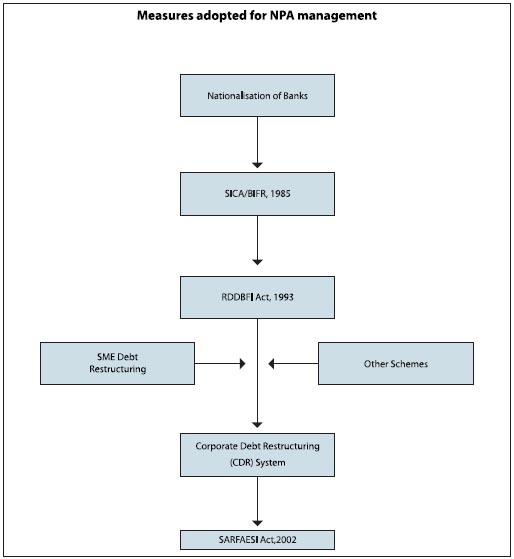

The SARFAESI Act has been largely perceived as facilitating asset recovery and reconstruction. Since Independence, the Government has adopted several ad-hoc measures to tackle sickness among financial institutions, foremost through nationalisation of banks and relief measures. Over the course of time, the Government has put in place various mechanisms for cleaning the banking system from the menace of NPAs and revival of a healthy financial and banking sector. Some of the notable measures in this regard include

- Sick Industrial Companies (Special Provisions) Act, 1985 or SICA: To examine and recommend remedy for high industrial sickness in the eighties, the Tiwari committee was set up by the Government. It was to suggest a comprehensive legislation to deal with the problem of industrial sickness. The committee suggested the need for special legislation for speedy revival of sick units or winding up of unviable ones and setting up of quasi-judicial body namely; Board for Industrial and Financial Reconstruction (BIFR) and The Appellate Authority for Industrial and Financial Reconstruction (AAIRFR) and their benches. Thus in 1985, the SICA came into existence and BIFR started functioning from 1987

The objective of SICA was to proactively determine or identify the sick/potentially sick companies and enforcement of preventive, remedial or other measures with respect to these companies. Measures adopted included legal, financial restructuring as well as management overhaul. However, the BIFR SARFAESI ACT 2002: An Assessment process was cumbersome and unmanageable to some extent. The system was not favourable for the banking sector as it provided a sort of shield to the defaulting companies.

- Recoveries of Debts due to Banks and Financial Institutions (RDDBFI) Act, 1993: The procedure for recovery of debts to the banks and financial institutions resulted in significant portions of funds getting locked. The need for a speedy recovery mechanism through which dues to the banks and financial institutions could be realised was felt. Different committees set up to look into this, suggested formation of Special Tribunals for recovery of overdue debts of the banks and financial institutions by following a summary procedure. For the effective and speedy recovery of bad loans, the RDDBFI Act was passed suggesting a special Debt Recovery Tribunal to be set up for the recovery of NPA. However, this act also could not speed up the recovery of bad loans, and the stringent requirements rendered the attachment and foreclosure of the assets given as security for the loan as ineffective.

- Corporate Debt Restructuring (CDR) System: Companies sometimes are found to be in financial troubles for factors beyond their control and also due to certain internal reasons. For the revival of such businesses, as well as, for the security of the funds lent by the banks and FIs, timely support through restructuring in genuine cases was required. With this view, a CDR system was established with the objective to ensure timely and transparent restructuring of corporate debts of viable entities facing problems, which are outside the purview of BIFR, DRT and other legal proceedings. In particular, the system aimed at preserving viable corporate/businesses that are impacted by certain internal and external factors, thus minimising the losses to the creditors and other stakeholders. The system has addressed the problems due to the rise of NPAs. Although CDR has been effective, it largely takes care of the interest of bankers and ignores (to some extent) the interests of borrower’s stakeholders. The secured lenders like banks and FIs, through CDR merely, address the financial structure of the company by deferring the loan repayment and aligning interest rate payments to suit company’s cash flows. The banks do not go for a one time large write-off of loans in initial stages.

- SARFAESI ACT 2002: By the late 1990s, rising level of Bank NPAs raised concerns and Committees like the Narasimham Committee II and Andhyarujina Committee which were constituted for examining banking sector reforms considered the need for changes in the legal system to address the issue of NPAs. These committees suggested a new legislation for securitisation, and empowering banks and FIs to take possession of the securities and sell them without the intervention of the court and without allowing borrowers to take shelter under provisions of SICA/BIFR. Acting on these suggestions, the SARFAESI Act, was passed in 2002 to legalise securitisation and reconstruction of financial assets and enforcement of security interest. The act envisaged the formation of asset reconstruction companies (ARCs)/ Securitisation Companies (SCs).

Provisions of the SARFAESI Act

The Act has made provisions for registration and regulation of securitisation companies or reconstruction companies by the RBI, facilitate securitisation of financial assets of banks, empower SCs/ARCs to raise funds by issuing security receipts to qualified institutional buyers (QIBs), empowering banks and FIs to take possession of securities given for financial assistance and sell or lease the same to take over management in the event of default.

The Act provides three alternative methods for recovery of NPAs, namely:

- Securitization: It means issue of security by raising of receipts or funds by SCs/ARCs. A securitisation company or reconstruction company may raise funds from the QIBs by forming schemes for acquiring financial assets. The SC/ARC shall keep and maintain separate and distinct accounts in respect of each such scheme for every financial asset acquired, out of investments made by a QIB and ensure that realisations of such financial asset is held and applied towards redemption of investments and payment of returns assured on such investments under the relevant scheme.

- Asset Reconstruction: The SCs/ARCs for the purpose of asset reconstruction should provide for any one or more of the following measures:

- the proper management of the business of the borrower, by change in, or take over of, the management of the business of the borrower

- the sale or lease of a part or whole of the business of the borrower

- rescheduling of payment of debts payable by the borrower

- enforcement of security interest in accordance with the provisions of this Act

- settlement of dues payable by the borrower

- taking possession of secured assets in accordance with the provisions of this Act.

- Exemption from registration of security receipt: The Act also provides, notwithstanding anything contained in the Registration Act, 1908, for enforcement of security without Court intervention: (a) any security receipt issued by the SC or ARC, as the case may be, under section 7 of the Act, and not creating, declaring, assigning, limiting or extinguishing any right, title or interest to or in immovable property except in so far as it entitles the holder of the security receipt to an undivided interest afforded by a registered instrument; or (b) any transfer of security receipts, shall not require compulsory registration.

The Guidelines for SCs/ARCs registered with the RBI are:

- act as an agent for any bank or FI for the purpose of recovering their dues from the borrower on payment of such fees or charges

- act as a manager between the parties, without raising a financial liability for itself;

- act as receiver if appointed by any court or tribunal

Apart from above functions any SC/ARC cannot commence or carryout other business without the prior approval of RBI.

The Securitisation Companies and Reconstruction Companies (Reserve Bank) Guidelines and Directions, 2003

The Reserve Bank of India issued guidelines and directions relating to registration, measures of ARCs, functions of the company, prudential norms, acquisition of financial assets and related matters under the powers conferred by the SARFAESI Act, 2002.

Defining NPAs: Non-performing Asset (NPA) means an asset for which:

- Interest or principal (or instalment) is overdue for a period of 180 days or more from the date of acquisition or the due date as per the contract between the borrower and the originator, whichever is later;

- interest or principal (or instalment) is overdue for a period of 180 days or more from the date fixed for receipt thereof in the plan formulated for the realisation of the interest of the assets

- Interest or instalment is overdue on expiry of the planning period, where no plan is formulated for the realisation of the

- any other receivable if it is overdue for a period of 180 days or more in the books of the SC or ARC.

Provided that the Board of Directors of an SC or ARC may, on default by the borrower, classify an asset as a NPA even earlier than the period mentioned above.

Registration:

Every SC or ARC shall apply for registration and obtain a certificate of registration from the RBI as provided in SARFAESI Act;

A Securitisation Company or Reconstruction Company, which has obtained a certificate of registration issued by RBI can undertake both securitisation and asset reconstruction activities;

Any entity not registered with RBI under SARFAESI Act may conduct the business of securitisation or asset reconstruction outside the purview of the Act.

Net worth of Securitisation Company or Reconstruction Company: Net worth is aggregate of paid up equity capital, paid up preference capital, reserves and surplus excluding revaluation reserve, as reduced by debit balance on P&L account, miscellaneous expenditure (to the extent not written off ), intangible assets, diminution in value of investments/short provision against NPA and further reduced by shares acquired in SC/ARC and deductions due to auditor qualifications. This is also called Owned Fund. Every Securitisation Company or Reconstruction Company seeking the RBI’s registration under SARFAESI Act, shall have a minimum Owned Fund of Rs 20 mn.

Permissible Business: A Securitisation Company or Reconstruction Company shall commence/undertake only the securitisation and asset reconstruction activities and the functions provided for in Section 10 of the SARFAESI Act. It cannot raise deposits.

Some broad guidelines pertaining to Asset Reconstruction are as follows:

- Acquisition of Financial Assets: With the approval of its Board of Directors, every SC/ARC is required to frame, a ‘Financial Asset Acquisition Policy’, within 90 days of grant of Certificate of Registration, clearly laying down policies and guidelines which define the; norms, type, profile and procedure for acquisition of assets,

- valuation procedure for assets having realisable value, which could be reasonably estimated and independently valued;

- plan for realisation of asset acquired for reconstruction

The Board has powers to approve policy changes and delegate powers to committee for taking decisions on policy/proposals on asset acquisition.

- Change or take over of Management/ Sale or Lease of Business of the Borrower: No SC/ARC can takeover/ change the management of business of the borrower or sale/lease part/whole of the borrower’s business until the RBI issues necessary guidelines in this behalf.

- Rescheduling of Debt/ Settlement of dues payable by borrower: A policy for rescheduling the debt of borrowers should be framed laying the broad parameters and with the approval of the Board of Directors. The proposals should to be in line with the acceptable business plan, projected earnings/ cash flows of the borrower, but without affecting the asset liability management of the SC/ARC or commitments given to investors. Similarly, there should be a policy for settlement of dues with borrowers.

- Enforcement of Security Interest: For the sale of secured asset as specified under the SARFAESI Act, a SC/ARC may itself acquire the secured assets, either for its own use or for resale, only if the sale is conducted through a public auction.

- Realisation Plan: Within the planning period a realisation plan should be formulated providing for one or more of the measures including settlement/rescheduling of the debts payable by borrower, enforcement of security interest, or change/takeover of management or sale/lease of a part or entire business. The plan should clearly define the steps for reconstruction of asset within a specified time, which should not exceed five years from the date of acquisition.

Broad guidelines with regards to Securitisation are as follows:

- Issue of security receipts: A SC/ARC can set up trust(s), for issuing security receipts to QIBs, as specified under SARFAESI Act. The company shall transfer the assets to the trust at a price at which the assets were acquired from the originator. The trusteeship remains with the company and a policy is formulated for issue of security receipts.

- Deployment of funds: The company can sponsor or partner a JV for another SC/ARC through investment in equity capital. The surplus available can be deployed in G-Sec or deposits in SCBs.

- Asset Classification: The assets of SC/ARC should be classified as Standard or NPAs. The company shall also make provisions for NPAs.

Issues under the SARFAESI

Right of Title

A securitisation receipt (SR) gives its holder a right of title or interest in the financial assets included in securitisation. This definition holds good for securitization structures where the securities issued are referred to as ‘Pass through Securities’. The same definition is not legally inadequate in case of ‘Pay through Securities’ with different tranches.

Thin Investor Base

The SARFAESI Act has been structured to enable security receipts (SR) to be issued and held by Qualified Institutional Buyers (QIBs). It does not include NBFC or other bodies unless specified by the Central Government as a financial institution (FI). For expanding the market for SR, there is a need for increasing the investor base. In order to deepen the market for SR there is a need to include more buyer categories.

Investor Appetite

Demand for securities is restricted to short tenor papers and highest ratings. Also, it has remained restricted to senior tranches carrying highest ratings, while the junior tranches are retained by the originators as unrated pieces. This can be attributed to the underdeveloped nature of the Indian market and poor awareness as regards the process of securitization.

Risk Management in Securitisation

The various risks involved in securitisation are given below:

Credit Risk: The risk of non-payment of principal and/or interest to investors can be at two levels: SPV and the underlying assets. Since the SPV is normally structured to have no other activity apart from the asset pool sold by the originator, the credit risk principally lies with the underlying asset pool. A careful analysis of the underlying credit quality of the obligors and the correlation between the obligors needs to be carried out to ascertain the probability of default of the asset pool. A well-diversified asset portfolio can significantly reduce the simultaneous occurrence of default.

Sovereign Risk: In case of cross-border securitization transactions where the assets and investors belong to different countries, there is a risk to the investor in the form of non-payment or imposition of additional taxes on the income repatriation. This risk can be mitigated by having a foreign guarantor or by structuring the SPV in an offshore location or have a neutral country of jurisdiction

Collateral deterioration Risk: Sometimes the collateral against which credit is sanctioned to the obligor may undergo a severe deterioration. When this coincides with a default by the obligor then there is a severe risk of non-payment to the investors. A recent example of this is the sub-prime crisis in the US which is explained in detail in the following sections.

Legal Risk: Securitisation transactions hinge on a very important principle of “bankruptcy remoteness” of the SPV from the sponsor. Structuring the asset transfer and the legal structure of the SPV are key points that determine if the SPV can uphold its right over the underlying assets, if the obligor declare bankruptcy or undergoes liquidation.

Prepayment Risk: Payments made in excess of the scheduled principal payments are called prepayments. Prepayments occur due to a change in the macro-economic or competitive industry situation. For example in case of residential mortgages, when interest rates go down, individuals may prefer to refinance their fixed rate mortgage at lower interest rates. Competitors offering better terms could also be a reason for prepayment. In a declining interest rate regime prepayment poses an interest rate risk to the investors as they have to reinvest the proceedings at a lower interest rate. This problem is more severe in case of investors holding long term bonds. This can be mitigated by structuring the tranches such that prepayments are used to pay off the principal and interest of short-term bonds.

Servicer Performance Risk: The servicer performs important tasks of collecting principal and interest, keeping a tab on delinquency, maintains statistics of payment, disseminating the same to investors and other administrative tasks. The failure of the servicer in carrying out its function can seriously affect payments to the investors.

Swap Counterparty Risk: Some securitisation transactions are so structured wherein the floating rate payments of obligors are converted into fixed payments using swaps. Failure on the part of the swap counterparty can affect the stability of cash flows of the investors.

Financial Guarantor Risk: Sometimes external credit protection in the form of insurance or guarantee is provided by an external agency. Guarantor failure can adversely impact the stability of cash flows to the investors.